Samples

We have successfully solved thousands of problems for clients. Here we show a few samples of how our work looks like:

Problem 1

A perfectly competitive firm has total revenue and total cost curves given by:

TR = 100Q

TC = 5,000 + 2Q + 0.2 Q2

a. Find the profit-maximizing output for this firm.

b. What profit does the firm make?

Answer: The profit function is given by

We differentiate to get:

The maximum profit is

The profit function is shown below:

Problem 2:

Assume that the demand

curve for bicycles in ;

and the supply curve for bicycles in NYC during the Fall is given by the

following curve,

.

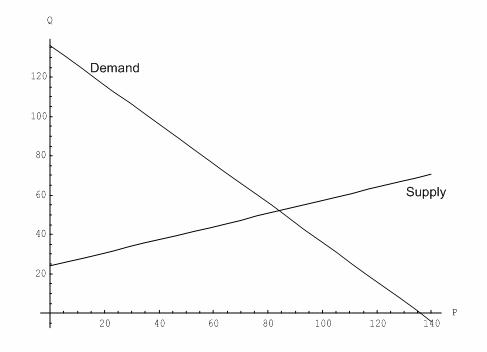

a) What is the choke price? What is the slope of the demand curve? What is the slope of the supply curve?

Answer: In order to find the choke price we solve:

The slope of the demand curve is ,

and the slope of the supply curve is

.

b) Graph the supply and demand curves for the market of bicycles in NYC during the Fall.

Answer: We have the following graph:

c)

What

is the equilibrium price and quantity in the market for bicycles in

Answer: By intersecting the demand and supply curve we get:

The equilibrium quantity is computed as

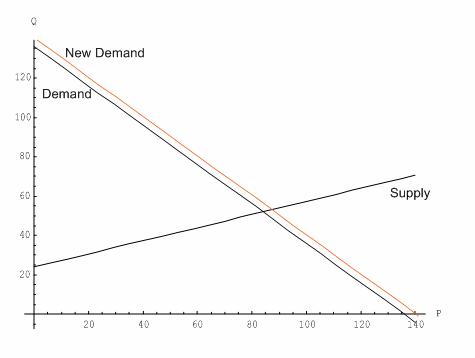

d) Fall has started in NYC. Unexpectedly, the weather turns out to be quite warm. Happy New Yorkers decide to spend more time biking around. As result, the original demand curve for bicycles in the Fall increases by 4 bicycles at every price. What is the new demand curve? Show it in the graph in (a).

Answer: The new demand is

In the new graph we have

e) What is the new equilibrium price and quantity?

Answer: Now we solve:

The new equilibrium quantity is

f) Why doesn't the new equilibrium quantity you found in (e) also increase by 4 bicycles? Briefly explain in words.

Answer: The new equilibrium will not be obtained in general by adding the amounts of units that demand was shifted, because it also depends on the interaction with the supply curve.

Topics

We can help with the following topics:

Some interesting economics resources

Don forget to add our site to your bookmarks

The benefits of getting homework help

There are many situations in which our services could be beneficial to you. Maybe you are in a time crunch, or you need to double check your econ solutions, for example.

Hundred of Satisfied Customers

We have successfully helped hundreds of customers, as we keep developing a strong trust relationship with each of our customers.

Payment Methods

Your payment is absolutely safe, as we use Paypal as our payment processors. You can pay with Paypal or with a credit or debit card